Which Account Saves You More Taxes: the Roth IRA or the Traditional IRA?

The Tax Cuts and Jobs Act (TCJA), passed in December 2017, reduced individual income tax rates temporarily until 2025. As a result, most Americans ended up paying less federal income taxes in 2018 and 2019 than in previous years.

However, starting in 2026, the tax rates will revert to those that existed up to 2017. The TCJA also provides for many of its other provisions to sunset in 2015. Effectively, Congress attempted to take away with one hand what it was giving with the other. Unless Congress acts to extend the TCJA past 2025, we need to expect a tax increase then. In fact, in a recent Twitter survey, we found that most people actually expect taxes to go up.

Some people hope that Congress will extend those lower TCJA tax rates beyond 2026. Congress might just do that. However, planning on Congress to act in the interest of average taxpayers could be a perilous course of action! Hope is not a plan!

Roth vs. Traditional IRAs

Given the reality of today’s comparatively low taxes, how can we best mitigate the TCJA’s scheduled tax increase? One way could be to switch some retirement contributions from Traditional IRA accounts to Roth IRA accounts from 2018 to 2025, and changing back to Traditional IRA accounts in 2026 when income tax brackets increase again. While we may not be able to do much about the 2026 increase, we can still work to reduce our lifetime taxes through planning.

Roth IRA accounts are well known for providing tax-free growth and retirement income within specific parameters. The catch is that contributions must be made with earned income that has been taxed already. In other words, Roth accounts aren’t exactly tax-free, they are merely taxed differently.

On the other hand, Traditional IRA retirement accounts are funded with pretax dollars, thereby reducing taxable income in the year of contribution. Then, distributions from Traditional IRA retirement accounts are taxed as income.

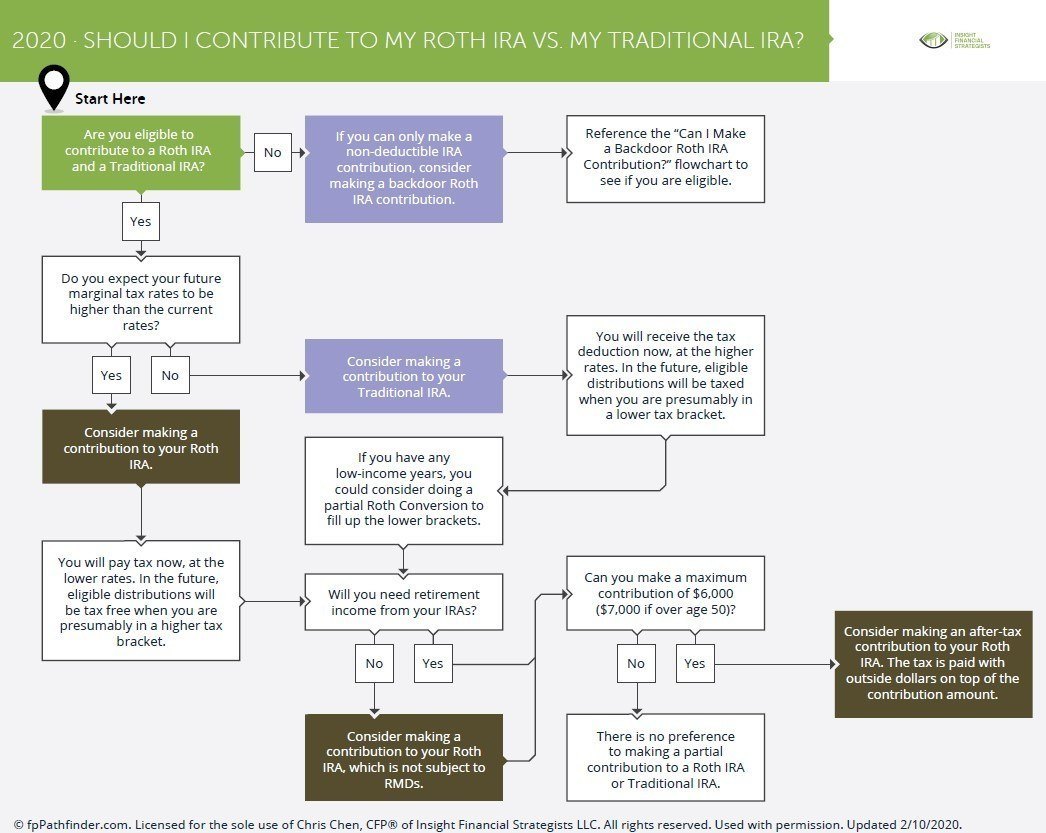

Thus, it is not always clear whether a Roth IRA contribution will be more tax effective than a Traditional IRA contribution. One of the critical considerations before deciding to contribute to a Roth IRA or a Roth 401(k) or to a Traditional IRA or Traditional 401(k) is the difference in income tax rates between contributing years and retirement years. If your projected tax rate in retirement is higher than your current tax rate, then you may want to consider Roth IRA contributions. If, on the other hand, your current tax rate is higher than your projected tax rate in retirement, contributing to a Traditional account may reduce your lifetime taxes.

The following flowchart can provide you with a roadmap for deciding between these two types of retirement accounts. Please let us know if we can help clarify the information below!

Other Considerations

There can be considerations other than taxes before deciding to invest through a Roth IRA account instead of a Traditional IRA account. For instance, you may take an early penalty-free distribution for a first time home purchase from a Roth. Or you may consider that Roth accounts are not subject to Required Minimum Distributions in retirement as their Traditional cousins are. Retirees value that latter characteristic in particular as it helps them manage taxes in retirement and for legacy.

However, the tax benefit remains the most prominent factor in the Roth vs. Traditional IRA decision. To make the decision that helps you pay fewer lifetime taxes requires an analysis of current vs. future taxes. That will usually require you to enlist professional help. After all, you would not want to choose to contribute to a Roth to pay fewer taxes and end up paying more taxes instead!

As everyone’s circumstances will be different, it would be beneficial to check with a Certified Financial Planner® or a tax professional to plan a strategy that will minimize lifetime taxes, taking into account future income and projected taxes.

Check out our other posts on Retirement Accounts issues:

Is the new Tax Law an opportunity for Roth conversions?

Rolling over your 401(k) to an IRA

Doing the Solo 401k or SEP IRA Dance

Tax season dilemma: invest in a Traditional or a Roth IRA

Roth 401(k) or not Roth 401(k)