Should You Buy An Annuity?

Annuities are a popular retirement planning device. According to Investment News, sales broke a record in 2018. Yet, they continue to be misunderstood. There are several types of annuities, with fixed, fixed indexed, and variable being some of the most common. Unfortunately, annuities are so complex, that salespeople often have difficulty communicating their values and shortcomings to clients. It is sometimes said, humorously, that the greatest value of an annuity is the steak dinner that it comes with.

Joking aside, the point is that annuities are complex and most of their benefits are intangible, except for the steak. As a client, you will eventually have to decide that if you are not going to become an expert with annuities, you will have to trust a salesperson.

Annuities have value. However, their value must be balanced with costs and lost opportunity considerations. In addition to the direct costs of the annuity, like “mortality and expense”, the expense ratio of the investments or the costs of the “riders”, and indirect opportunity costs what are the value of the benefits you might be giving up to get an annuity?.

First, what does an annuity get you?

Fixed Income

The most commonly advertised benefit of an annuity is fixed income. The insurance company that sells and manages the annuity will be paying you periodically, usually monthly, for the rest of your life (usually). That payment is presented as fixed: it will never decrease. Obviously, that is appealing to a lot of people: finally a financial instrument with some safety built in.

Rarely does the salesperson point out the obvious: the periodic payment amount will never increase either.

Why does it matter yo have your payment increase? In an age where people ought to be planning for retirement for 20 or 30 years or more, a periodic payment that does not increase is basically a payment that continuously loses value to inflation. While you may not notice it from one year to the next, inflation is pernicious: it will slowly eat away your purchasing power.

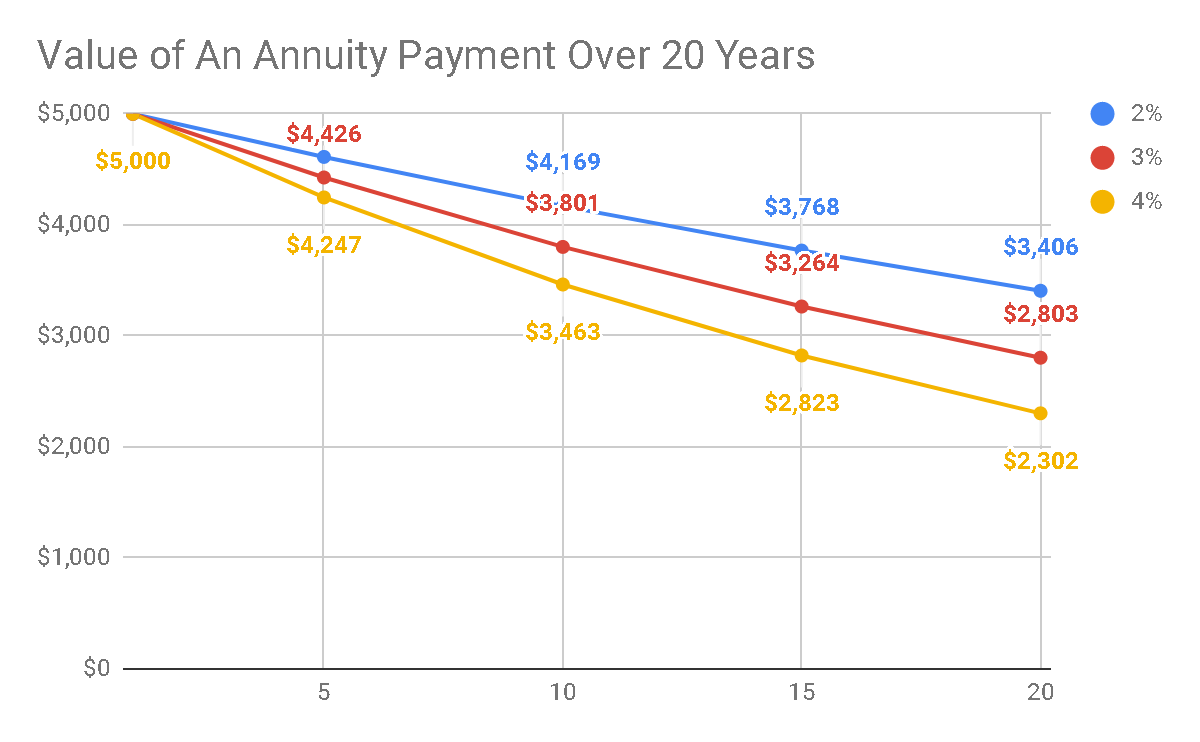

For instance, the table below shows that with inflation of 3%, the value in today’s dollars of a $5,000 annuity payment that you might receive today goes down to $2,803 in 20 years. In other words, you would be losing almost $2,200 of purchasing power automatically. Needless to say, this is something that you would want to know before buying the annuity.

Source: Insight Financial Strategists LLC

Tax Advantage

Also, annuities are Tax-advantaged. Americans love tax-advantaged investments, almost as much as they like tax-free investments. That is a key point to note: the money that you contribute to an annuity is not taxable when it distributes in retirement because, presumably, you have already paid taxes on it. Therefore, when the annuities distribute in retirement, part of the distribution is your own money that comes back to you tax-free. The gains, however, come back to you taxable as ordinary income.

Now, how does the tax treatment of annuities compare to other methods of investing, like for example investing in equities and fixed income outside of an annuity? As with annuities, contributions to your investment are not taxed again when they are distributed. However, your gains will usually be taxable as capital gains. This is important because for many people capital gains tax rates are lower than ordinary income tax rates. In other words, you may very well be paying more taxes by putting your money in an annuity than if you had invested outside of it if the right circumstances are met.

Guarantee

Another attractive benefit of annuities is that the payment amounts are Guaranteed. Financial Planners are not usually able to say that anything is guaranteed, because we do not know the future. However, financial salespeople can say that about annuities, because the benefits are guaranteed by the insurance company. Obviously, that is a very powerful statement, especially in the absence of comparable guarantees for traditional investment products.

The bottom line is that traditional investments are not guaranteed. We know from watching the market or hearing about it on TV that anything can happen. In particular, the stock market can drop.

Hence if we could protect ourselves from the risk of the stock market going down, it would obviously be a good thing. We know that in any given year the market could go down. In fact, according to Logan Kane, on any random day, we have a 47 percent chance of stocks falling and a 53% chance of stocks rising. In any given year, we have a 75% chance of stocks rising.

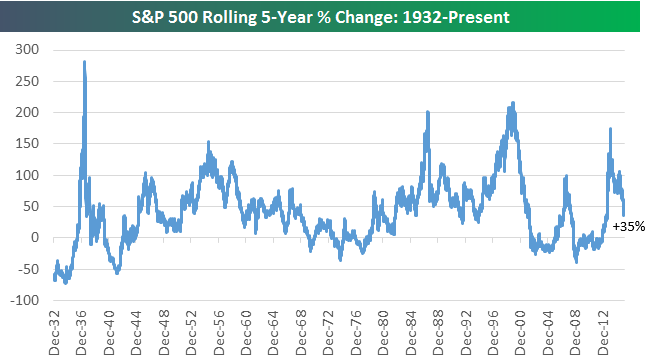

We also know that on average the stock market goes up. In fact, even when it goes down, we know that in any rolling five year period it will also go up as demonstrated with the S&P500 on the following graph.

Source: bespokepremium.com

Therefore, when we protect ourselves against the downsides of the stock market with annuities we give up a lot of upside opportunity cost in return.

Investments

Annuity companies tend to be shy about disclosing how your contributions are invested, except for variable annuities where the regulatory disclosure requirements are well developed. Variable annuities are invested in a mix of stock and bond funds. You can get a thorough description in their disclosure document.

Otherwise, insurance companies will rather have a root canal than tell you how their fixed annuities are invested. Perhaps it does not matter since the insurance company guarantees the payments. Maybe we don’t need to know.

Fixed index annuities are another matter. These instruments allow for the potential for growth. Mind you, in the typical words of a self-described “industry-leading financial organization”, ” your money is not actually invested in or exposed to the market”.

They can get away with this statement because it is, most likely, technically true. However, in order to make the returns that they claim that their annuities can make, the insurance companies have to invest in something more than cash. Fixed index annuities put their money, your money, in derivatives: stock options and futures. Technically, it saves you stock market volatility by being outside of it. Instead, you get derivatives market volatility which is even greater.

This has to be one of the most misleading sales pitches that financial salespeople make about fixed index annuities. Still, if the insurance company guarantees the returns, maybe it’s okay anyway?

Costs

Lastly, what about the costs??

Insurance companies tend to be less than forthcoming about the costs of their annuities, except when regulations force them to disclose them. For instance, variable annuities typically disclose a lot of information. When you read the prospectus you will find that it discloses various kinds of fees: administration, mortality and expense, mutual fund subaccount, turnover ratio, and death benefit being some of the most common. According to the Motley Fool, you might find that the total ongoing cost of your variable annuity can be anywhere from 2.46% to 5.94% a year.

Disclosure requirements for fixed and fixed index annuities are much less developed, which may be why insurance companies don’t typically disclose them. However, disclosure notwithstanding, there is definitely a cost that goes to paying your salesperson’s commission or the complicated options and futures strategies on your fixed index.

Value

The primary value of annuity products is not in the income or guarantee or tax benefit that they provide. The primary value of annuities is that they absorb risks that you as an investor are not willing to take in the market. Annuities give you a guaranteed fixed income. In exchange, they limit the possibility of growth in your capital or your income.

They do that by balancing your risks with other people like you. As we suspect, most of us will not have an average life expectancy. We are either above average or below average. As Bill Sharpe, a Nobel prize winner in economics reminds us, buying an annuity allows us to share those risks, and for those of us who are above average, an annuity may well be a great bargain.

As the organizer of the annuity party, the insurance company absorbs some of the risks as well. When we buy an annuity, we are transferring the risk of investing on our own to the insurance company. If the insurance fails in its investments, it commits to paying us anyway. That is valuable, but does the benefit need to cost that much? Could it be overpriced?

Annuities can provide incredible value. However, the simplicity of providing guaranteed monthly income is well overtaken by the complexity, direct costs and the opportunity cost. It is important to understand what you are getting and what you are giving up with an annuity, You can make sure that it meets your needs first by getting advice that is in your best interest by a fee-only financial planner. You can find one at NAPFA or XYPN. Both are organizations of Certified Financial Planners that are committed to giving you advice that is in your best interest.