Table of Contents

Should You Retire with a Mortgage

Introduction

Transitioning to retirement while holding a mortgage isn’t ideal, yet it happens more often than most people think.

According to Investopedia 32% of seniors 65-74 had a mortgage in 2022. And according to the Congressional Research Service, the amount of mortgage debt held by senior households has increased more than 500% over the past three decades ending in 2016. So, if you are transitioning to your golden years with a mortgage in tow, you are not alone.

Most financial planners offer the standard advice that it is not financially prudent to enter retirement with mortgage debt or any other debt, for that matter. That makes sense, of course. Debt creates an additional expense burden that must be satisfied and a liability that may eventually require the liquidation of an asset.

However, the data above shows that it is becoming increasingly difficult to retire without a mortgage. And there are situations where it makes sense. Debt provides leverage and options to achieve goals that might be difficult to reach otherwise.

Could it make sense?

It may sound obvious, but it bears reminding that getting a loan means that you can preserve other assets for other purposes. And many times, that makes sense.

For example, if your assets are tied in an illiquid investment, you may need the cash to buy that vacation house on Martha’s Vineyard. We don’t have to think exotic to find illiquid investments in our portfolios. Most retirement accounts, including 401(k)s and IRAs, have a form of limited liquidity. Because they are taxed at distribution, there are practical limits to the size of the distribution that is advisable to take in any given year. Taking too much may result in more taxes than you are comfortable with. Other assets, such as private equity, also have limited liquidity. A mortgage on your primary residence may be a solution in this kind of scenario.

Some also have their wealth tied in other illiquid investments, such as real estate or private placements. A mortgage may allow you the flexibility to enjoy life without liquidating assets (and paying taxes).

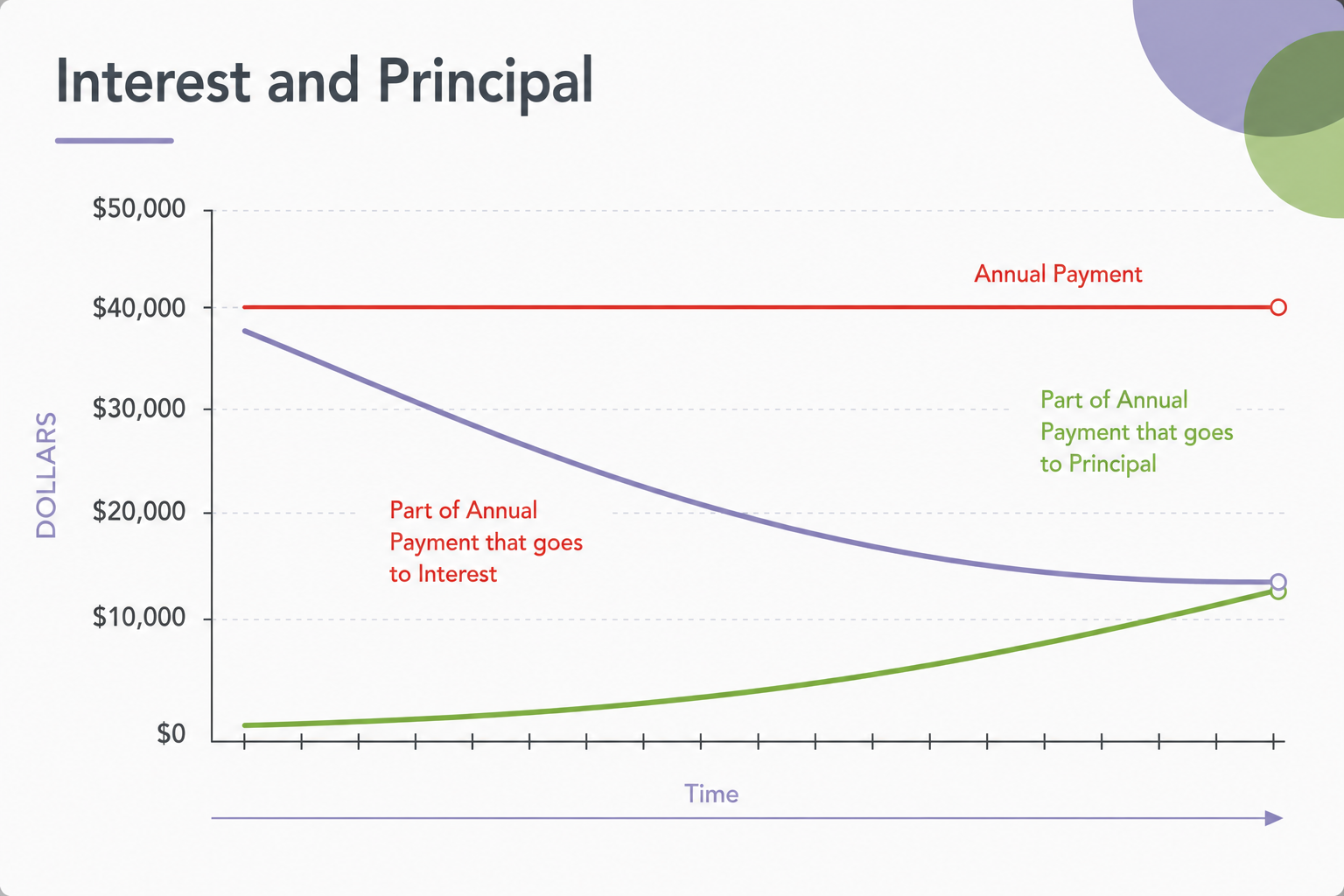

It also depends on the age of the mortgage. A key motivation to pay off a mortgage is to save interest payments. That is especially true at the beginning of the life of a mortgage. Then, most of the payments go to interest instead of principal. However, because mortgages amortize over time, most of the interest in the later life of a mortgage goes to the principal, with a decreasing percentage going to interest.

Graph 1: Principal and Interest over the Life of a Mortgage

This doesn’t mean that you cannot save interest payments by paying early; it just means that the amount that can be saved decreases with every payment. In Graph 1 above, the area below the red line represents the percentage of monthly payments going to interest. As more payments are made, you move to the right of the graph, and an increasing amount goes to principal. It may be less expensive to continue mortgage payments than to pay early, depending on the specific financial situation (1).

For example, if you have a 30-year, 3% mortgage on $300,000, your monthly payments for principal and interest will be $1,264.81. If you keep the mortgage for all 30 years and make all the payments on time, you will end up paying $155,332.36 in interest payments. However, if you pay off the mortgage halfway through after 15 years, maybe when you start retirement, you will be saving only $44,514.47. To save that $44K, you would have to pay the remaining principal of $183,151. Counting estimated federal and state taxes, if applicable, you might have to withdraw $250,000 from retirement accounts to make that one payment (2). In other words, the $44K saved on interest could well be dwarfed by nearly $70K paid in taxes. Not to mention the lost growth in the retirement account’s value.

Table 1: Principal and Interest with 30 years and 15 years

Table 1: Principal and Interest with 30 years and 15 years

Every situation is different, of course. Maybe not all of the money needs to come from retirement accounts. Maybe it can come from an unneeded Required Minimum Distribution, in which case there is no incremental tax cost, since taxes have to be paid anyway (3).

There are a lot of maybes! It is best to pass them by your Certified Financial Planner.

Are There Other Benefits?

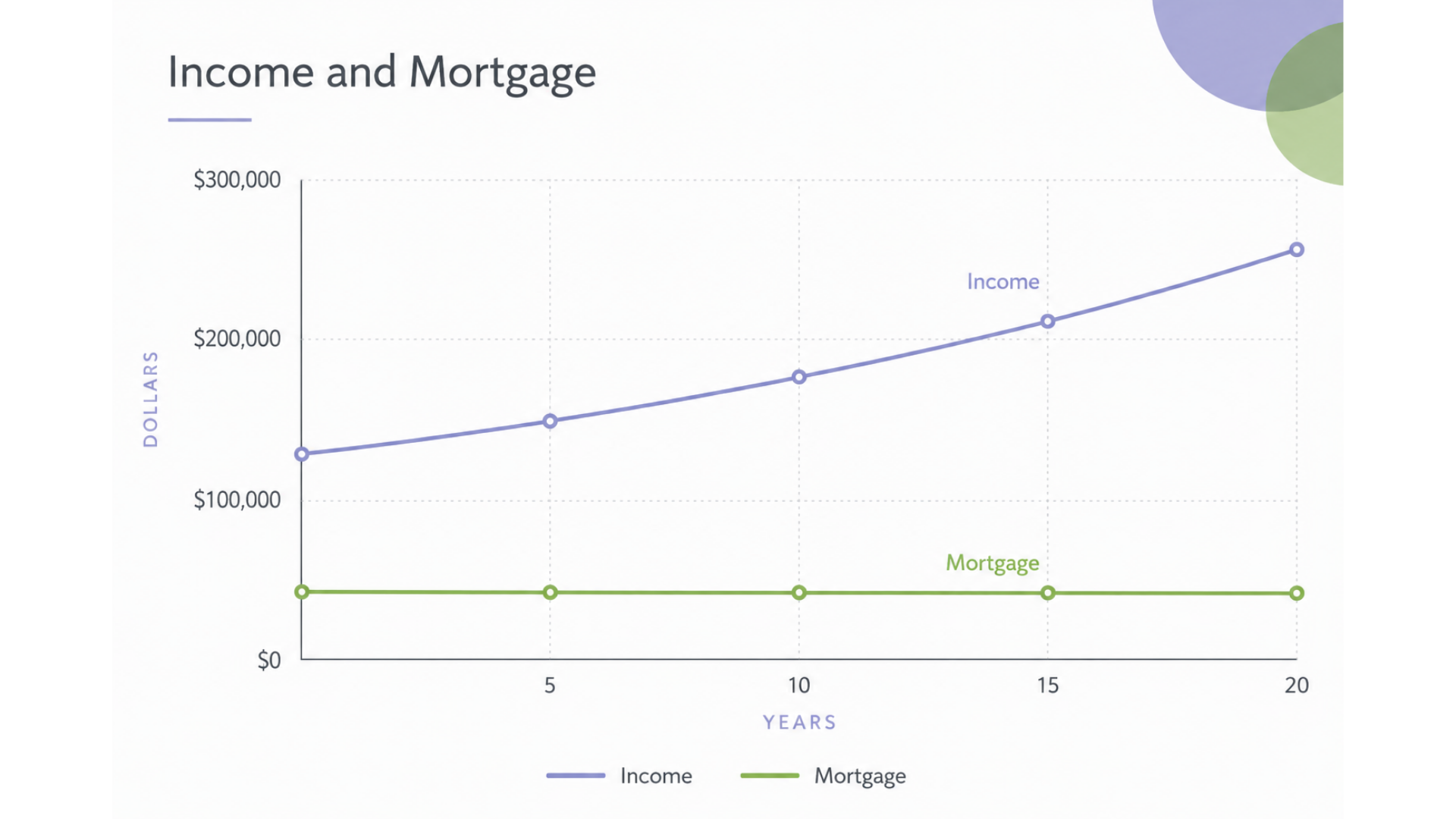

In most cases, mortgage interest is fixed. If you obtained your mortgage before the rate increases of the recent past, the interest portion is relatively low as interest rates have since increased. If your income is projected to increase, then the percentage that goes to mortgage payments will decrease. Over time, the mortgage becomes a smaller part of your budget. Graph 2 below shows a case with a fixed mortgage payment and increasing income over 30 years. Over time, a mortgage payment that may feel tight at the beginning will become less stressful in a monthly budget.

Keep Your Debt Under Control

However, there are criteria to observe. The first is that the debt payments should fit within your budget. If you have such debt, you should be able to pay it comfortably out of your retirement income. If it is not comfortable, other solutions should be considered.

That can be confusing because people with retirement income continue to take from their retirement savings, such as Required Minimum Distributions. The key is to make sure with your Certified Financial Planner that it fits within the plan.

Home equity loans (HELOCs) may be different in several ways. The first is that there is often no amortization schedule, meaning that the HELOC will not get paid off before maturity unless you make a concerted effort. Another difference is that HELOCs usually carry variable interest, unlike most regular mortgages, which have a fixed interest. Thus, they can be dangerous in an environment of increasing rates.

When is it Acceptable to Retire With Mortgage Debt?

Few people plan to enter retirement with a mortgage. However, it happens.

Parents may refinance a mortgage to fund college for their teenager. But unfortunately, with the rising cost of college and parents’ sense of responsibility, many Moms and Dads end up in the situation where a mortgage is the most convenient and, potentially, the less expensive source of cash.

People often move before or during retirement, buy a new house, and end up with a mortgage. That could be due to downsizing or a move to a sunnier state. In this circumstance, people often have a plan for their accumulated equity. Some of that could go to pay other debt, such as student loans or PARENT loans. Or it could go to investment, maybe even a real estate investment, such as a rental or vacation home.

In some cases, some of the equity from the house that was just sold goes to helping to fund retirement at a faster clip, i.e., spending. There are so many things that we can do with money!

As a result, there are situations in which it is perfectly acceptable to retire with mortgage debt. The key consideration is ensuring that it fits within your overall financial plan.

Potential Benefit

There may be a long-term benefit: with a fixed interest rate, your mortgage payments will remain fixed while inflation pushes your income and the value of your home upward.

And in today’s inflationary environment, with inflation close to mortgage interest rates levels, the value of a monthly mortgage payment decreases over time simply because money devalues due to inflation. At the same time, as illustrated in Graph 2, income often increases, even in retirement, lightening the burden of mortgage payments over time.

In plain terms, this means it gradually becomes less expensive to pay a mortgage throughout retirement as long as that debt is locked in at a fixed rate and income rises.

Graph 2: Relationship between income and mortgage payments

What Not to do in the Context of Retiring With Mortgage Debt

If you still feel it is prudent to pay off your mortgage as you transition to retirement, take some time to review the pros and cons.

If you pay off the mortgage early in its life without drawing from retirement accounts, you could be saving a lot of interest payments. Although, as noted previously, a low mortgage interest rate in a high inflation environment may well pay for itself.

Consider the Opportunity Cost of Paying off Your Mortgage

There can be a significant opportunity cost to paying off a mortgage early. It is even greater when paying off a mortgage that has aged for years or decades. For example, suppose you are collecting Social Security, pension payments, or other income adjusted for inflation, and you own no or few liquid post-tax assets. In that case, paying off the mortgage would have to come from liquidating assets and result in a higher tax bill or lost investment growth. In these cases, it might not make financial sense to pay off the entirety of the mortgage in one fell swoop.

Doing so could leave you without an emergency fund or liquidity.

How to decide?

When in doubt, run the numbers. Meet with a Certified Financial Planner to estimate the potential returns from investments or the cost to liquidate. Then, compare those anticipated returns with the interest that accumulates from holding your mortgage debt during retirement, paying the monthly minimum as you have for years or decades. If your investment returns are likely to outpace the money lost from the mortgage interest accumulation, it may be in your financial interest to use your financial nest egg to invest rather than pay off the balance of your mortgage, keeping in mind, of course, that there are no guarantees in investment.

Don’t let Emotions Override Logic

Like most homeowners, you are yearning to own your home outright and fire your bank as a co-owner. And if you are like most retirees, having a mortgage will make you uncomfortable.

You may also be tired of paying hundreds or thousands of dollars each month simply to have a roof over your head that you can call your own.

However, it is a mistake to let mortgage debt, or any other money issue for that matter, become overly emotional. But, unfortunately, it is also hard not to.

Instead of paying a potentially steep financial price to eliminate your mortgage at the wrong time, take the logical approach by meeting with your Certified Financial Planner. Your financial planner will delve into the nuances of your unique financial situation and then detail the advantages and disadvantages of holding the mortgage until its term ends or paying it off as you segue into retirement.

(1): It does depend on the financial situation. Check with your Certified Financial Planner.

(2): Taxes are estimated for illustrative purposes. Depending on the specific situation, they could be higher or lower.

(3): Because RMDs are mandatory, taxes will be paid regardless of what the taxpayer does with the money. Effectively, taxes are not relevant to that particular calculation.