Incorporating Sustainable Investing Principles Into Your Portfolio

The term “sustainable investing” is often used interchangeably with “socially responsible investing”. In general, these terms describe an approach to investing that combines traditional financial methods to portfolio construction with the desire to simultaneously create positive societal outcomes.

The term “sustainable investing” is often used interchangeably with “socially responsible investing”. In general, these terms describe an approach to investing that combines traditional financial methods to portfolio construction with the desire to simultaneously create positive societal outcomes.

What might these societal outcomes be? The industry has gravitated to three broad areas of impact – Environmental, Social and Governance (ESG).

We are all exposed to these various areas in our daily lives and many of us care deeply about some of these issues. For the most part, we have channeled our beliefs into action through charitable giving and volunteering efforts.

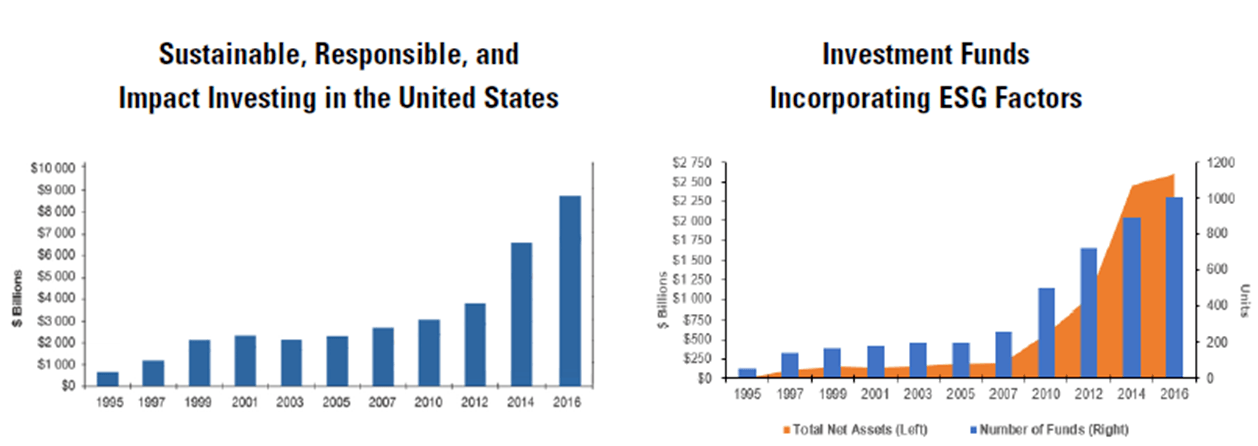

But a new way of “doing good while also doing well” has emerged in the last few years. Investment strategies have been designed to deliver competitive financial returns while also impacting society in a positive manner.

Sounds too good to be true? Large institutional investors have been able to achieve both financial and societal returns for a long time, but only in recent times have investment strategies been designed to enable individual investors to achieve the same objective.

How did sustainable investing get started? In its early days socially responsible or what we now call sustainable investing took an exclusionary view to investing. For example, tobacco companies were often excluded from portfolio mandates. Another, probably more extreme example involved the divestment of South African investments during the apartheid era. Companies selected under this form of exclusionary screening had to meet a minimum threshold of “do no harm” but that was about it.

How has sustainable investing changed in the last few years? More recently, investors have looked at ways to create positive social outcomes within their financial portfolios. The focus has shifted toward emphasizing investments with the dual objective of superior risk adjusted financial returns along with demonstrably positive environmental, societal and/or governance outcomes.

“Doing good while doing well” is the basic rationale why investors are increasingly interested in enhancing how they manage their portfolios by including non-financial metrics such as environmental, societal and governance factors.

Besides ethical and moral motivations, why have investors suddenly become so interested in sustainable approaches to investment management? Simple – self-interest combined with the realization that currently disclosed financial metrics are insufficient to properly account for the long-term sustainability and valuation of companies.

Large and small investors have woken to the fact that environmental issues such as climate change and carbon emissions have significant implications for our global well-being as well as for the long-term financial health of companies. This is the E in ESG.

Investors are also becoming very interested in the societal impacts of corporate behavior. Issues such as workers’ rights, gender and diversity policies and human rights in general. This represents the S in ESG. For example, recent sexual harassment scandals at various media companies highlight the impact of non-financial events on corporate valuation.

Probably the oldest way of using non-financial criteria to evaluate companies involves the area of corporate governance. This is the G in ESG. Board composition, executive compensation practices and sustainability disclosure criteria are just three areas of increasing investor attention.

Is it possible to achieve competitive returns and also deliver a significant impact? Research indicates that “doing good while doing well” is achievable if properly implemented.

One of the concerns of early investors in SRI approaches was that excluding companies deemed to be “bad actors” would significantly restrict one’s investment opportunities and returns would commensurately suffer.

Recent empirical studies show that returns need not suffer especially when risk-adjusted.

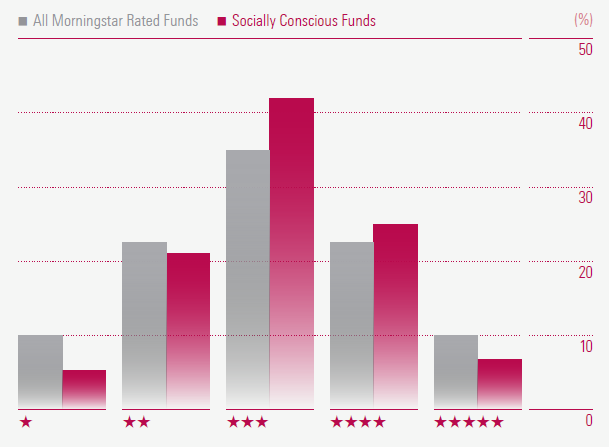

Research from Morningstar depicted below highlights a segment of socially responsible funds compared to the broad universe of US equity mutual funds. The general conclusion is that socially conscious funds tend to have a higher representation among 3 and 4 star funds and lower proportions in the tails.

While not a ringing endorsement, the Morningstar research at least points out that there is no empirical reason to suspect that socially conscious funds underperform the general universe of US mutual funds.

Research generally shows that sustainable investing strategies do no harm, but can you do better? Yes, when the issues examined have a clear link to financial performance. This relates to the issue of materiality.

Research generally shows that sustainable investing strategies do no harm, but can you do better? Yes, when the issues examined have a clear link to financial performance. This relates to the issue of materiality.

Certain ESG issues are important from a societal standpoint but have a tenuous relationship to financial metrics such as company profitability or asset valuation. For example, preserving the Costa Rican Toucan is a worthwhile societal goal, but few publicly traded companies have a direct financial link to such an effort.

On the other hand, global warming has a direct effect on the severity of hurricanes and directly impact the financial performance of companies in the insurance and construction industries among others. Such an effect would be deemed material and of great consequence to individual investors with allocations to sustainable investing strategies.

Recent research by Harvard professors Khan, Sarafeim and Yoon identified a large variation in long-term measures of company financial success when evaluating companies on material ESG metrics. Their conclusion is that companies with superior sustainability practices outperform companies with poor practices. *

How can individual investors incorporate sustainable investing strategies into their overall portfolios? Our take is that properly constructed portfolios incorporating financial as well as non-financial ESG criteria are competitive on a risk-adjusted basis over short holding periods while providing significant positive upside over the long-term.

Our belief is that investors will benefit long-term from lower levels of business risk in their holdings as well as potentially higher stock returns.

Companies with superior ESG practices tend to provide greater transparency in their disclosures, be better prepared to deal with adverse events when they happen, and be more open to adapting their business models around environmental, social and governance issues likely to be material over the long-term.

Are sustainable investing strategies different from traditional approaches? The same risk-return balancing issues that apply to any investment portfolio apply to an approach using sustainability criteria. The biggest difference at the moment occurs at the implementation stage.

Implementing ESG portfolios requires additional research and caution. While a growing universe of investment vehicles exist in the form of mutual and exchange traded funds there are wide differences in liquidity, composition and cost. Properly conducting due diligence on the various sustainable investing offerings requires an above-average experience and know-how of financial materiality issues.

At Insight Financial Strategists we have done significant research on sustainable investing and believe that these strategies are here to stay and will deliver on the goal of “doing good while doing well”.

Please schedule a time to discuss with us your financial planning and investment needs and how a sustainable investing approach might fit your requirements.

Note: The information herein is general and educational in nature and should not be construed as legal, tax, or investment advice. Views expressed are the opinions of Insight Financial Strategists LLC as of the date indicated, based on the information available at that time, and may change based on market and other conditions. We make no representation as to the accuracy or completeness of the information presented. This communication should not be construed as a solicitation or recommendation to buy or sell any securities or investments. To determine investments that may be appropriate for you, consult with your financial planner before investing. Market conditions, tax laws and regulations are complex and subject to change, which can materially impact investment results.

* “Corporate Sustainability: First Evidence on Materiality” by Mozaffar Khan, George Serafeim, and Aaron Yoon, Harvard Business School Working Paper No. 15-073, March 2015.

Individual investor performance may vary depending on asset allocation, timing of investment, fees, rebalancing, and other circumstances. All investments are subject to risk, including the loss of principal.

Insight Financial Strategists LLC is a Registered Investment Adviser.