5 Risk Factors for Investors in 2018 – 3 Bad and 2 Good

2017 came and went without nary a whimper. None of the big concerns at the end of the previous year happened or at least global capital markets did not seem to be disturbed by much of anything.

2017 came and went without nary a whimper. None of the big concerns at the end of the previous year happened or at least global capital markets did not seem to be disturbed by much of anything.

Stocks went up in a straight line, bonds did ok, volatility was super low and at the end of the year exuberant expectations were in full bloom as everybody and their aunt became fixated on Bitcoin.

The global economy keeps doing well and memories of the 2008 Financial Crisis are receding. Consumer sentiment remains upbeat.

Being an investor is wonderful when markets are calm and statements show gains month after month. Everybody is an investment genius. We forget how painful it is when capital markets experience stress and things get a bit crazy.

The mental picture I use is that of flying. The six hour trip from Boston to LA is great when it is all smooth sailing. The plane seems to be flying itself and you pay more attention to the movie you are watching than thinking about the age of the aircraft or training of the pilot and crew.

But the first time there is a little air bump and maybe lighting strikes your plane you immediately tense up and fix your gaze on the crew. Are they calm? Do they seem competent? Is this their first rodeo?

You form a mental image of what you want your pilot to look like. Calm and collected for starters. But mainly experienced. We all want to see Captain Sully at the helm.

Clearly, we all would love smooth capital markets forever. But the close friend of return is always uncertainty. The two are inseparable even though they may not always be in direct contact. In times of turbulence you want experience at the helm and a solid understanding of how the two are intertwined.

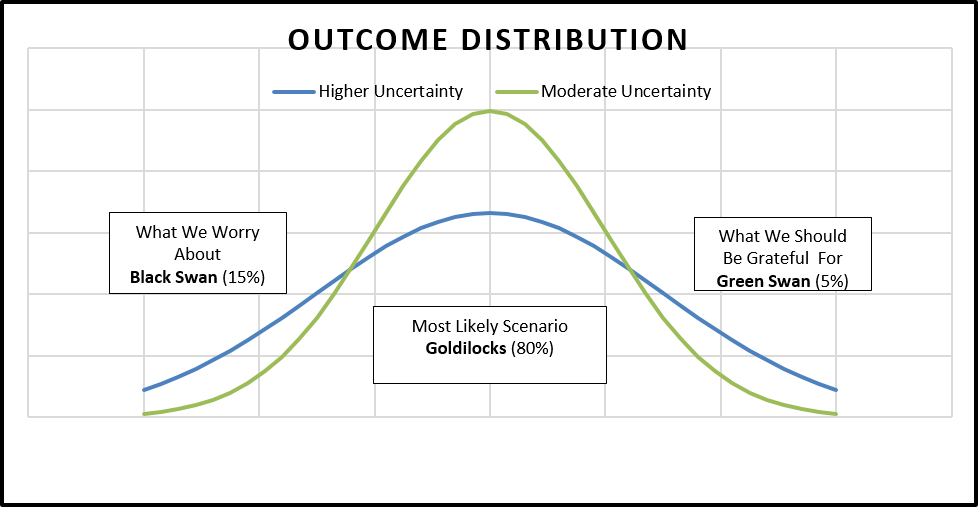

How do we think of uncertainty in the capital markets? There are as many ways of defining uncertainty as there are opinions as to who the greatest quarterback in history is (we all know it is Tom Brady, right) but without hopefully appearing too cavalier we think that it is useful to think of uncertainty as a normal distribution of potential outcomes.

We fear the left tail where things go terribly wrong, we accept the middle of the distribution as textbook risk/return, and we think that our own brilliance (just joking) has led us to the right tail of the distribution.

In 2017 equities, in particular, had a monster year with the S&P 500 up over 25% and many international markets up even more. The year turned out much better than expected. What do we expect for this coming year?

Our baseline assessment is fairly benign as we discussed last month in our Capital Market Overview. A quick review is in order.

We expect equities to again do better than bonds. We also expect international assets to outperform domestic strategies. We expect robust global growth. Our most likely scenario for this year is for continued growth, subdued inflation and no major equity or bond market meltdown. In our judgement there is about an 80% probability that such a scenario plays out in 2018.

On the downside we expect the low volatility that has accompanied capital markets recently to once again revert back to risk on/off.

[pullquote align=”normal”]Our baseline assessment is fairly benign [/pullquote]

We expect to see more large jumps in market prices caused by low probability events lurking in the left hand side of the distribution. The press calls these events Black Swans. Our best assessment is that there is about a 15% probability of seeing a Black Swan event in 2018.

On the other end of the uncertainty distribution you have what we call Green Swans – events, low in probability that when they happen are wildly positive for investors. We attach a 5% chance of experiencing such extreme positive events over the current calendar year

What could cause a Black Swan in 2018?

1. An inflation spike caused by a sustained rally in commodity prices

Inflation in the US is currently running a bit above 2% and market participants do not expect to see any major revisions over the next two decades (see the Philadelphia Federal Reserve estimate of inflationary expectations).

In our view, forecast complacency has set in and the risks are to the upside. Traders would describe the low inflation trade as over-crowded. Maybe it is time to re-think what happens if the consensus turns out to be wrong.

The immediate effect of an upward spike in inflation would be a rise in bond yields. Equities would probably take a short-term hit but the primary casualties would be found in the fixed income market.

What could cause a sustained surge in commodity prices? One, could be a supply disruption say in the oil market. Another could be related to the resurgence of global growth and continued demand for commodities such as iron ore and copper. Third, a depreciating US dollar leading to commodity price inflation.

2. A spike in capital market turmoil caused by a geo-political blowup

The blowup could be anywhere in the world but most political commentators point to North Korea and Iran as the most likely centers of conflict.

Another possibility is a cyberattack endangering public infrastructure facilities especially if it is sovereign sponsored. Third, Jihadi terrorism on a large scale and on high profile targets. And last, the outcome of the Special Counsel investigation into Russian meddling.

All of these events have blowup potential. While the probability of any of these events happening in 2018 is low, the magnitude of the capital market response is likely to be large and negative especially for equity markets. Global economic growth would also, no doubt, loose some of its momentum.

3. An avalanche of bond defaults in the apparel and retail industries in the US and/or a debt bomb crisis in China

It is no secret that the US apparel and retail sectors are going through massive consolidation driven in part by the shift to online shopping. It is widely acknowledged that the US retail market is over-built.

The number of apparel and retail companies expected to disappear is higher today than in 2008 during the Financial Crisis. Read here for a list of apparel and retailers at risk.

According to the Institute of International Finance global debt hit a record last year at $233 trillion. Debt levels as a percentage of global GDP are higher today compared to 2007. Figuring prominently in the debt discussion is China.

Source: IIF, IMF, BIS

The IMF recently issued a warning to the Chinese authorities about the rapid expansion of debt since the 2008 Financial Crisis. The rapid expansion in debt has funded lesser quality assets and poses stability risk for global growth according to the IMF.

Estimates by Professor Victor Shi at UC San Diego put Chinese total non-financial debt at 328 percent of GDP. Other estimates are even higher leading to an overall picture of rising liabilities and numerous de facto insolvencies. The robust GDP growth in China and the tacit understanding of the monetary authorities of the extent of the problem will hopefully keep the wolves at bay.

The implications of a debt scare for investors would be quite dire. Investors have had plenty of experience with debt crisis in recent years – Greece and Cyprus come to mind as Black Swan events that temporarily destabilized global capital markets. A Chinese debt scare would no doubt be of greater impact to global investors. Emerging market debt spreads would certainly blow up.

What about the right hand tail of the uncertainty distribution – the Green Swans?

These are wildly positive events for investors that carry a low probability of happening. What type of Green Swan events could we hope for that would lead capital markets to yet another year of phenomenal returns?

1. Positive global growth surprise possibly brought on by the recently enacted US tax reform

The US is the largest economy in the world and still remains a significant engine of global growth. Could we be surprised by a spurt in US economic growth this year?

According to the Conference Board US real GDP is expected to growth 2.8% in 2018. Could we see 4% growth? The President certainly hopes so. Not that likely. The last time that US GDP growth was above 4% was in 2000.

What could give us the upside scenario for growth? Maybe a jump in consumer spending (representing 2/3 of GDP) driven by real wage growth and lower taxes.

Another possibility is a surge in investment by US corporations driven by cash repatriations and recently enacted corporate incentives.

We view both scenarios as likely but providing only a marginal boost to growth. As they say we remain cautiously optimistic, but would not bet the farm on this.

2. A spurt in exuberant expectations driven by the cryptocurrency craze

Fear of missing out (FOMO) takes over repricing all investments remotely tied to the cryptocurrency craze along the way. We saw a similar scenario play out in 1999 in the final stages of the Technology, Media and Telecom (TMT) bubble.

In those days TMT stocks were no longer priced according to traditional fundamentals but instead on the idea that laggard investors would buy into the craze and drive prices even higher. Lots of investors succumbed to FOMO in the final stages of the bubble.

The recent price action of Bitcoin and most other cryptocurrencies has a similar feeling to the ending stages of the TMT bubble. It is almost as if Bitcoin and its cousins are being discussed along with the latest Powerball jackpot.

No doubt fortunes have been and will continue to be made in cryptocurrencies. Blockchain technology which underlies the crypto offerings is here to stay, but we worry about the lack of investor education and the speed of the price action in late 2017. Whatever happened to Peter Lynch’s “buy what you know” approach?

What would be our best estimate for capital markets should the cryptocurrency craze gain further momentum in 2018? First, technology stocks would continue out-performing. Chip suppliers such as Nvidia and AMD would continue to see massive growth.

Companies adopting blockchain technologies would see their valuations increase disproportionally. In general, animal spirits would be unleashed onto the capital markets making rampant speculation the order of the day. The primary beneficiary would be equity investors.

Conclusion:

History tells us that it is almost certain that after 8 years of an economic expansion and stock market recovery we should see an outlier type of event in 2018. What shape and form it will take (or Swan color) we don’t know.

Preparing for tail risk events is very expensive and under most scenarios not worth bothering with.

Black Swans create great distress for investors, but the opportunity cost of playing it too safe is especially high today given prevailing interest rates that fail to keep up with inflation.

The fear of missing out (FOMO) during Green Swan events is also a powerful investor emotion. Again playing it too safe can result in many lost opportunities for capturing significant market up moves.

Investing in capital markets is all about weighting these probabilities and focusing on a small number of key research-driven fundamental drivers of risk and return.

How you structure your portfolio and navigate the uncertainties of capital markets is important to your long-term financial health. Putting a financial plan in place and having an experienced Captain Sully-type as your captain during times of turbulence should reassure investors in meeting their long-term goals.

Note: The information herein is general and educational in nature and should not be construed as legal, tax, or investment advice. Views expressed are the opinions of Insight Financial Strategists LLC as of the date indicated, based on the information available at that time, and may change based on market and other conditions. We make no representation as to the accuracy or completeness of the information presented. This communication should not be construed as a solicitation or recommendation to buy or sell any securities or investments. To determine investments that may be appropriate for you, consult with your financial planner before investing. Market conditions, tax laws and regulations are complex and subject to change, which can materially impact investment results.

Individual investor performance may vary depending on asset allocation, timing of investment, fees, rebalancing, and other circumstances. All investments are subject to risk, including the loss of principal.

Insight Financial Strategists LLC is a Registered Investment Adviser.