[thrive_headline_focus title=”A Hypothetical Case of Fear vs Greed Tradeoffs” orientation=”left”]

How our brain works:

We all think that we are fully rational all the time but in reality the way our brains operate that is not always the case.

One of the key functions of the brain is self-defense. When the brain perceives danger it makes automatic adjustments to protect itself. When it perceives discomfort it seeks to engage in an action that removes the stress.

In his book “Thinking Fast and Slow” Nobel Prize Winner Daniel Kahneman explains how we all have a two way system of thinking that we use to make decisions. He labels the two components as System 1 (Thinking Fast) and System 2 (Thinking Slow).

System 1 is automatic, fast responding and emotional. System 2 is slower, reflective and analytical.

Think of your System 1 as your gut reaction and your System 2 as your conscious, logical thought.

While we all like to think that our key life decisions are governed by our logical thought (System 2) research has shown that even major decisions are often driven by our gut feel.

Which System do we use to make a decision? That depends on the problem. If we have seen the problem many times before such as what to do when see a red light we default to our automatic System 1 thinking.

When we face a challenge or issue that we have not seen before or maybe infrequently we tend to use System 2, our more reflective and analytical capabilities.

Kahneman’s research shows that we spend most of our time in System 1. While most people think of themselves as being rational and deliberate in their decision making, the reality is that we often employ “short-cuts” or heuristics to make decisions.

Most of the time, these “short-cuts” work just fine but occasionally for more difficult or complex problems the impressions arrived from System 1 thinking can lead us astray.

Why? Above all else, System 1 thinking seeks to create quick and coherent stories based on first impressions. These impressions are a function of what our brain is sensing at that moment in time.

According to Kahneman, conclusions are easily reached despite often contradictory information as System 1 has little knowledge of logic and statistics. He calls this phenomenon – WYSIATI – for “what you see is all there is”.

The main implication from WYSIATI is that people often over-emphasize evidence that they are familiar with and ignore evidence that may be much more relevant to the problem at hand but that they are not fully aware of.

System 1 conclusions therefore may be biased and lead to decision “short-cuts” or heuristics that seriously impair the quality of a decision.

What makes making “money” decisions so hard?

When it comes to investing people often rely too much on System 1 or automatic thinking. The research shows that we are not infallible and we in fact often make behavioral mistakes. Sometimes we over-rely on our gut feel without properly evaluating the consequences of our actions.

Often our brain perceives of the dangers first and sends us a warning signal to be careful. Losing money puts us on red alert.

Behavioral finance research (for example in the book Nudge) has shown that losing money makes you twice as miserable as gaining the same amount makes you happy. People are loss averse.

Loss aversion makes people overvalue what they have due to a reluctance to incur any losses should they make a change. What they give up, sometimes unknowingly, is potential upside.Loss aversion creates inertia. Inertia often works against investors that overvalue the attractiveness of their current holdings.

There are different degrees of loss aversion. According to Prospect Theory, all investors value gains less than losses but some exhibit an extreme dislike for potential losses that significantly hinders their long-term wealth creation potential.

Nobody likes to lose money, but taking on risk in order to compound your hard earned savings is an integral feature of how capital markets work. You don’t get a higher reward unless you take additional risk.

Most investors know that stocks do better than bonds over the long-term but that the price of these higher returns is more risk. Investors also understand that bonds do better most of the time than simply purchasing a CD at the local bank or investing in a money market mutual fund.

But knowledge stored in your logical and analytical System 2 thinking does not always make it through in the face of stress or uncertainty.

People can become too risk averse for a couple of reasons:

- Case A: They let their fears and emotions guide their investment decision making and give disproportionate importance to avoiding any losses

- Case B: They fail to calibrate their expectations to the likely frequency of outcomes.

In Case A, investors seek the perceived safety of bonds often not realizing that as interest rates go up bonds can lose money. Or they simply pile into CD’s not realizing that their returns most often fail to keep up with inflation. Stocks are frowned upon because you can lose money.

Investors in Case A let their decisions be driven by emotion and fear and will over-value the importance of safety and under-value the importance of future portfolio growth. Their account balances will not go down much when capital markets experience distress, but neither will they go up much during equity bull markets.

In Case B investors mis-calibrate their expectations for various investment outcomes and the consequences can be as dire as in the first situation. Behavioral finance research has shown that investors frequently over-estimate the likelihood and magnitude of extreme events such as stock market corrections.

Investors often become fixated on what could happen should an equity market correction occur, but they fail to properly evaluate the likelihood and magnitude of such a correction in relation to historical precedents. They also importantly fail to properly calibrate the probability of observing a recovery after going through such a correction.

What are the implications for investors playing it too safe?

Let’s consider the case of investors currently working and saving a portion of their income to fund a long-term goal such as retirement. These individuals are in the accumulation phase of their financial lives.

Somebody in the accumulation phase will naturally worry more about how fast they can grow their portfolio over time and whether they will reach their “number”. People in the accumulation phase care primarily about their balances going up year after year. They are in “growth” mode.

The Hypothetical Setting:

To better illustrate this situation let’s look through the eyes of a recent college grad called Pablo earning $40,000 a year. Pablo is aware of the need to save part of his salary and invest for the long-term. He just turned 22 and expects to work for 40 years.

Pablo will also be receiving annual 2.5% merit salary increases which will allow him to save a greater amount each year in the future.

The Problem:

Pablo faces two key decisions – what percentage of his salary to save each year and the aggressiveness of his portfolio which in turn will determine its most likely return.

He is conflicted. He has never made this much money before and worries about losing money. He also understands that he alone is responsible for his long-term financial success.

Pablo knows that there is a trade off between risk and return but he wants to make a smart decision. His System 1 thinking is saying play it safe and don’t expose yourself to potential loses.

At the same time his rational and informed System 2 thinking is influenced by a couple of finance and economics classes he recently took while in college.

Pablo can succumb to automatic System 1 thinking and invest in a very conservative portfolio. Or he can rely on his System 2 thinking and invest in a higher risk and commensurately higher return portfolio.

One Alternative – Save 10% of his Income and play it safe investing

For simplicity sake assume that Pablo decides to put 10% of his salary into an investment fund. The fund consists primarily of high grade bonds such as those contained in the AGG exchange traded fund.

From the knowledge gained in his econ and finance classes Pablo estimates that this portfolio should return about 4% per year – a bit below the historical norm for bonds but consistent with market interest rates as of August 2018.

Pablo also understands that such a portfolio will have a bit of variability from year to year. He estimates that the volatility of this portfolio is likely to be about 6% per year. Again, this estimate is in line with current bond market behavior as of August of 2018.

He knows that this is a low risk, low return portfolio but the chances of this portfolio suffering a catastrophic loss are negligible. He is petrified of losing money so this portfolio might fit the bill.

How large could his portfolio be expected grow to over 40 years of saving and investing in this conservative manner? We built a spreadsheet to figure this out. We assumed a 4% portfolio return on principal, 2.5% annual salary increases and a half year of investment returns on annual contributions also at 4%. Remember that this is a hypothetical example with no guarantee of returns.

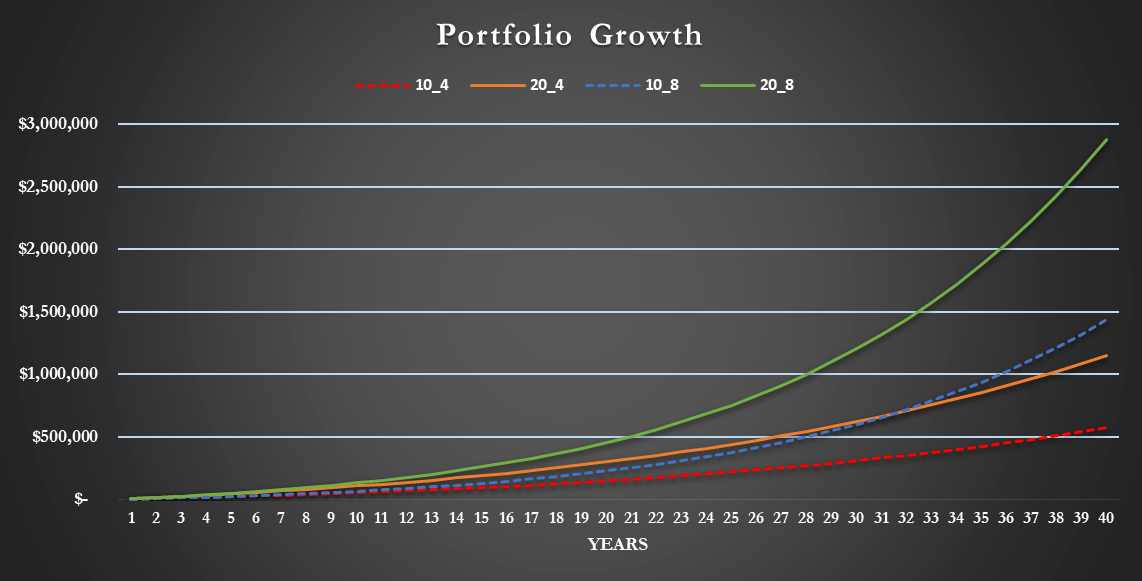

At the end of 40 years Pablo’s salary is assumed to have grown to $107,403 and his portfolio, invested in this conservative manner, would have a balance of $575,540. The growth of this portfolio (identified as 10_4) is shown in Figure 1. The naming convention for the portfolios corresponds to the savings rate followed by the assumed hypothetical rate of return on the strategy.

Figure 1

Source: Insight Financial Strategists, Hypothetical Example

Pablo knows that his portfolio will not exactly return 4% every year. Some years will be better, other years much worse but over the next 40 years the returns are likely to average close to 4%.

But Pablo does not feel comfortable just dealing in averages. If things go bad, how bad could it be?

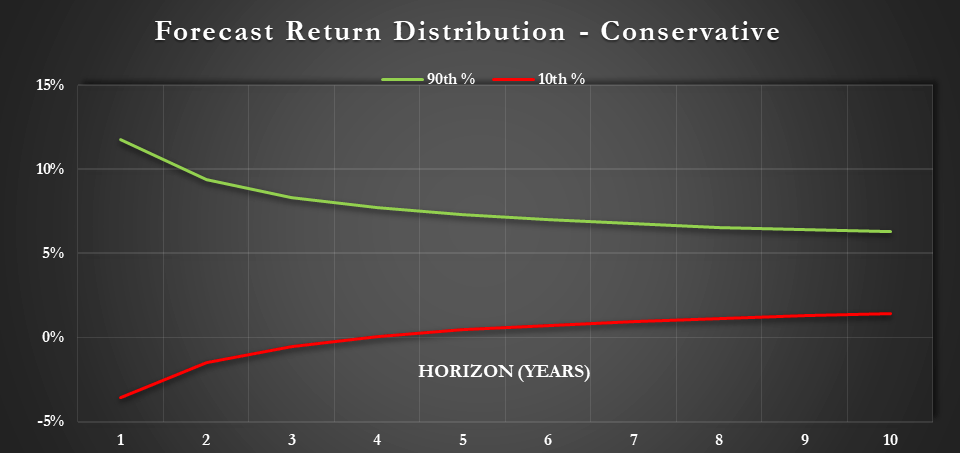

Given the volatility of this conservative portfolio there is a 10% chance of losing 3.6% in any given year. These numbers are calculated by Insight Financial Strategists based on an approximation of a log-normal simulation and are available upon request. Not catastrophic but nobody likes losing money.

Figure 2 shows the 90th and 10th probability bands for this conservative portfolio. These bands are estimated based on the expected average return of the portfolio and its volatility.

The actual portfolio return would be expected to lie about 2/3 of the time within these bands. In the short-term, say 1 to 2 years out, the portfolio returns are more unpredictable. Over longer horizons, the average return to this conservative portfolio should fall within much tighter bands given the assumed risk and return numbers in the log-normal simulation.

Based on the calculations, the average returns over ten years should range between 6.3% and 1.4% per annum. Clearly, even this conservative portfolio has some risk especially in the short-term, but over longer holding periods returns should smooth out.

Figure 2

Source: Insight Financial Strategists

Another Alternative – Save 20% of his Income and continue investing in a conservative portfolio

Assuming the same 2.5% annual salary increases, the final salary would have been the same but his nest egg would have grown to $1,151,080. Pablo keeps looking at Figure 1 (the 20_4 line representing a 20% savings rate invested at an assumed 4%) and starts thinking that maybe a bit of extra saving would be a very good thing.

He still has a 10% probability of being down 3.6% in any given year, but if his budget allows, he feels that he can forego some frills until later.

Now, Pablo is starting to get excited and wonders what would happen if he invested more aggressively, say in a variety of equity funds?

Yet Another Alternative – Keep saving the same amount but invest more aggressively

The likely returns would go up but so would his risk. He estimates that based on current market conditions and the history of stock market returns (obtained from Professor Damodaran of NYU) that this more aggressive portfolio should have about an 8% annual rate of return with a volatility of around 14% per year. These estimates are both a bit lower than the 1926-2017 average reflecting higher current (as of August 2018) valuations and lower levels of overall market volatility.

He is thinking that maybe by taking more risk in his portfolio during his working years he will be able to build a nest egg that may even allow him for some luxuries down the road.

He also knows that things do not always work out every year as expected. Pablo is pretty confident that 8% is a reasonable expectation averaged over many years, but how bad could it be in any given year?

A log-normal simulation was conducted using the assumed risk and return numbers – same approach as before.

Figure 3 shows the 90th and 10th percentile bands for this portfolio.

Figure 3

Source: Insight Financial Strategists

Given the volatility of this equity-oriented portfolio, there is a 10% chance of losing 9.2% in any given year (based on the simulations). Ouch, the reality of equity investing is starting to sink in for Pablo.

But Pablo is also encouraged to see that his returns in any given year are equally likely to be about 26% or higher. That would be nice!

Especially when it comes to equities there is a wide range of potential returns but over time these year by year fluctuations should average out to a much narrower range of outcomes. While our best estimate is that this portfolio will return on average 8% per year over a ten-year window the range of expected outcomes should be between a high of 12.9% and a low of 1.6%.

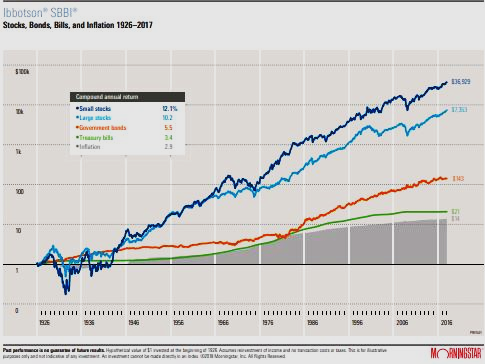

Pablo decides to research the history of stock, bond, and cash returns by reading our April Blog on Understanding Asset Class Risk and Return and looking at a chart of long-term returns from Morningstar (Figure 4).

Figure 4

Source: Morningstar

He is surprised to find that over the long-term equities do not seem as risky as he previously thought. He is also quite surprised by the wide gap in wealth created by stocks versus bonds and cash.

The research makes Pablo re-calibrate his expectations and he starts wondering whether the short-term discomfort of owning equities is worth it in the long run.

____________________________________________________________________

The “Aha!” Moment:

Pablo’s System 1 thinking is on high alert and his first thought after seeing how much he could lose investing in equities is to run back to the safety of the bond portfolio.

But something tells him to slow down a bit and think harder. This is a big decision for him and his System 2 thinking is kicking in. Before he throws the towel in on the equity-oriented portfolio he glances again at Figure 1 to see what might happen if he invests more aggressively.

What he sees astounds him. It is one thing to see compounding in capital market charts and yet another to see it in action on your behalf. Small differences over the short term amount to very large numbers over long periods of time.

If Pablo were to invest in the more aggressive portfolio there would be more hiccups over the years but his ending account balance should be $1,440,075 if he consistently put aside 10% of his salary every year.

If he saved 20% the ending portfolio balance would double in size.

Decision Time – Picking among the alternatives

Pablo is now faced with a tough decision. Does he play it safe and go with the conservative portfolio? Or, does he go for more risk hoping to end up with a much larger nest egg but knowing that the ride may be rough at times?

Beyond the numbers, he realizes that he needs to look within to make the best possible decision. His System 1 thinking is telling him to flee, but his System 2 thinking is asking him to think more logically about his choices. He also needs to deal with how much he is planning to save from his salary.

Fear versus Greed:

He needs to come to terms with how much risk he is willing to take and whether he can stomach the dips in account balance when investing in riskier assets. As Mike Tyson used to say, “Everybody has a plan until they get hit in the face”.

In structuring his investment portfolio Pablo needs to balance fear with greed. Paying attention to risk is absolutely necessary but always in moderation and in the context of historical precedents. If Pablo lets his fears run amuck he may have to accept much lower returns.

With the benefit of hindsight, he may come to regret his caution. On the other hand, the blind pursuit of greed and a disregard for risk may also in hindsight come back to bite him. Pablo needs to find that happy medium but only he can decide what is right for him. Risk questionnaires can help in this regard. Try ours if you like!

Consumption Today versus Tomorrow:

Pablo also needs to come to grips with how much current consumption he is willing to forego in order to save and invest. We live in an impulse oriented society. Spending is easy, saving is hard.

Saving is hard especially when you are starting out. On the other hand, over time the saving habit becomes an ingrained behavior. The saving habit goes a long way toward ensuring financial health and the sooner people start the better.

Will Pablo be able to save 10% of his salary? Or, even better will he be able to squeeze out some additional expenditures and raise his saving to 20%?

If possible Pablo should consider putting as much money in tax-deferred investment vehicles such as a 401(k). He should also have these contributions and any other savings automatically deducted from his paycheck. That way he won’t get used to spending that money. Pablo may come to see these deductions from his paycheck as a “bonus” funding future consumption.

“The greatest mistake you can make in life is to continually be afraid you will make one”

— ELBERT HUBBARD

___________________________________________

Lessons Learned:

This has been an eye-opening experience for our hypothetical friend Pablo. He was not expecting such a difference in potential performance. He now realizes the importance of maximizing saving for tomorrow as well as not succumbing to fear when investing for the long-term.

He has learned several invaluable lessons that also apply to individuals in the accumulation phase of their financial lives

Lesson 1: The Importance of Saving

- Delaying consumption today allows you fund your lifestyle in the future

- Saving even small amounts makes a big difference over the long-term

Lesson 2: The value of patience and a long-term perspective

- In the early years you may not notice much of a difference in portfolio values

- Keep saving and investing – disregard short-term market noise and stick to a plan

Lesson 3: Small differences in returns can amount to huge differences in portfolio values

- Seemingly tiny differences in returns can result in large differences in portfolio values

- Compounding is magic – take advantage of it when you can

Lesson 4: The importance of dealing with your fear of losing money

- Letting your first instinct to avoid risky investments dictate what you own will work against you

- Investing involves risk – best to manage rather than avoid risk

- The pain and agony of losing money in any given year is alleviated over the long term by the higher returns typically accruing to higher risk investments

Lesson 5: Investing in your financial education pays off

- Gaining a proper understanding of capital market relationships is an invaluable skill to possess

- Leaning on financial experts to expedite your learning is no different than when athletes hire a coach

____________________________________________________________________

Now what should you do?

Avoid all risks, save a lot and watch your investment account grow slowly but smoothly? Or, take some risk and grow your portfolio more rapidly but with some hiccups?

Are a couple of restless night’s worth the higher potential returns in your portfolio? On

Also, are you willing to delay some current consumption in order to invest for the future?

The answer depends on you – your needs, goals and especially your attitude toward risk and your capacity to absorb losses.

Interested in having the professionals at IFS identify your risk tolerance, time horizon, and financial needs? Please schedule a complimentary consultation here.

____________________________________________________________________

Disclaimer:

Much of the data used in these illustrations comes courtesy of Professor Aswath Domodaran from NYU and covers US annual asset returns from 1928 to 2017. Information presented herein is for discussion and illustrative purposes only and is not a recommendation or an offer or solicitation to buy or sell any securities. Views expressed are as of the date indicated, based on the information available at that time, and may change based on market and other conditions. References to specific investment themes are for illustrative purposes only and should not be construed as recommendations or investment advice. Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk.

This piece may contain assumptions that are “forward-looking statements,” which are based on certain assumptions of future events. Actual events are difficult to predict and may differ from those assumed. There can be no assurance that forward-looking statements will materialize or that actual returns or results will not be materially different from those described here.

Stock and bond markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Investing involves risk, including risk of loss.